How long is a piece of string? Economics is a notoriously hard subject to understand, let alone predict. While we would all like to know when the cost-of-living crisis will end, the truth is there’s no clear answer.

Our current inflationary crisis is particularly unique. Rather than there being a single cause for rising prices, many different issues are coming together at once to add to the pressure. Some of them are problems we’ve never really had to deal with before.

Stick with us though, as it’s not all bad, and some smaller sections of the economy could end up presenting investors with new opportunities.

What do we mean by “cost-of-living” and what defines a crisis?

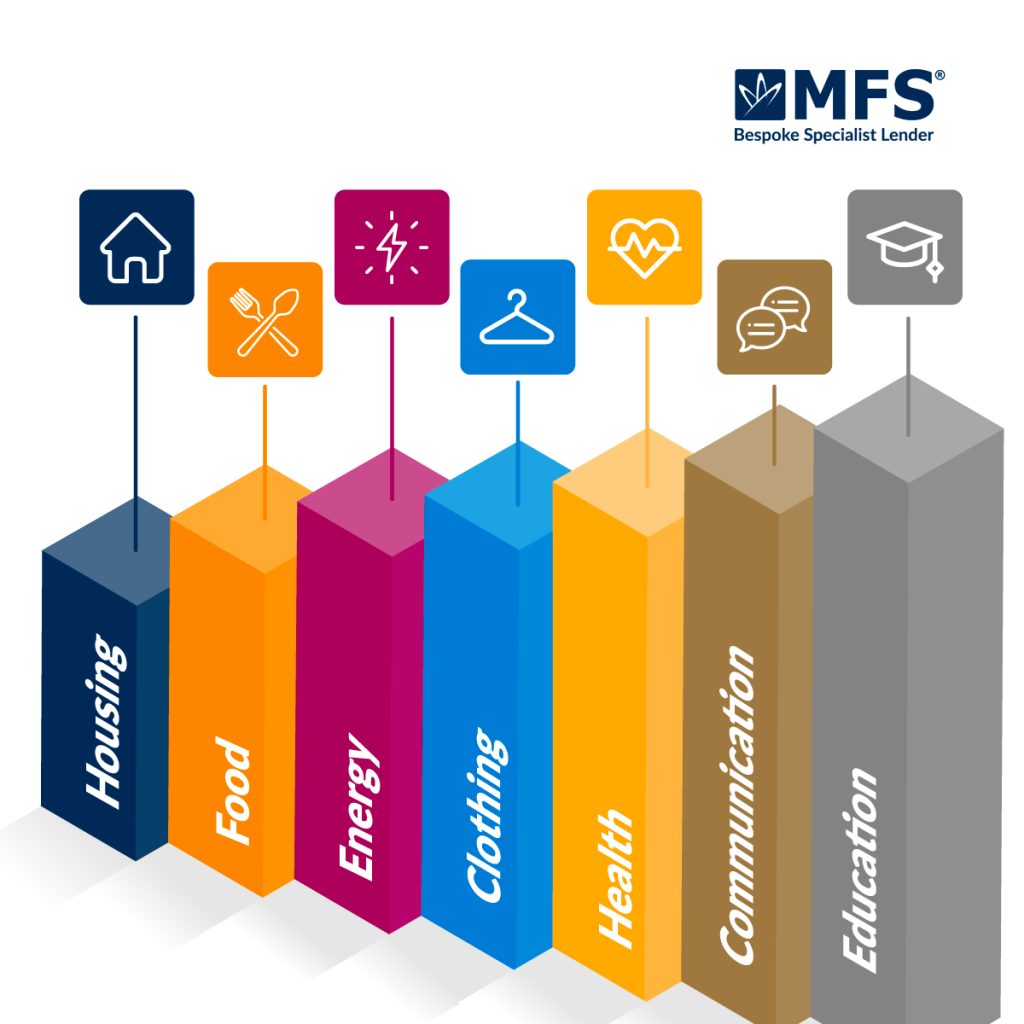

Before we investigate the question ‘when will the cost-of-living crisis end?’, we had better define exactly what it is we’re talking about. Generally, the cost-of-living refers to how much money you’ll need to cover the essentials. This usually includes housing costs, food, energy and the like.

In the UK, the consumer price index (CPI) is used as the official measure of inflation – a general increase in prices. The CPI is an average of several goods and services meant to reflect overall prices in the economy. Currently, it incorporates clothing, health, communication, education, and other elements.

A cost-of-living crisis refers to a period where these kinds of essentials become increasingly unaffordable. Consumer spending power is stretched, and wages don’t keep up with rising prices. The Bank of England aims to keep inflation at a sustainable 2% level. As it explains: “If inflation is too high or it moves around a lot, it’s hard for businesses to set the right prices and for people to plan their spending.

“But if inflation is too low, or negative, then some people may put off spending because they expect prices to fall. Although lower prices sounds like a good thing, if everybody reduced their spending then companies could fail and people might lose their jobs.”

Despite efforts to counteract rising prices though, both the CPI and the CPIH (the consumer prices index including owner occupiers’ housing costs) have skyrocketed since early 2021. In the last half of 2022, inflation regularly hovered around the 10% mark.

Source: Bank of England, ONS

What’s causing our current cost-of-living crisis?

We’ve just come out of a global pandemic, during which our government spent billions to keep our economy afloat. The bill for this is starting to come due.

What’s more, as we all tried to get back to normality following several lockdowns, demand for certain goods and services jumped. Oil and gas prices have risen, as have food, health, and clothing costs. Rising demand generally pushes prices higher.

Wages are rising, but not nearly enough to offset these price increases. Average wages, not including bonuses, rose by 5.7% in the three months to September 2022, compared to the same period in 2021. But, inflation reached 11.1% in October. Consumer spending power is struggling to play catch-up.

Most of these problems, at least in recent months, have been exacerbated by the war in Ukraine. As Russia invaded Ukraine, Western leaders issued economic sanctions to try and stop the aggression.

In response, Russia cut off its substantial gas supplies to Europe. Much of Europe has been dependant on Russian gas in the past and as that resource dried up, we were all left facing an energy crisis.

As 2023 approaches, many are still left wondering when will the cost-of-living crisis end. While there’s no clear-cut answer to this, positive signs are emerging. The worst of it may soon be behind us.

Source: BBC, The Institute for Government, ONS, CNBC

How to solve this crisis and what timeframes could we be looking at?

Comparisons between now and the 1970s are being made across the media at the moment. During that decade, inflation was running rampant, there was widespread industrial action, and stagflation ground us to a halt. All of this will sound familiar, but any comparisons with the past should be taken with a pinch of salt.

The world has never been more globalised. British consumers in the 1970s didn’t have the internet, quantitative easing, or the numerous other economic factors that affect us today.

Nevertheless, the last time we saw skyrocketing prices like this was back in the early 70s. To try and combat it, the Bank of England base rate was raised to 17% in 1979 – with hiking interest rates being a common tactic in bringing inflation under control.

This is likely a terrifying number for you to see, but it’s unlikely interest rates will reach that height again. In fact, we could see the cost-of-living crisis slowdown from next year.

Europe has learned from this difficult period. Efforts are being made to become less reliant on Russia for gas. The UK is looking towards the US and Germany for energy support and cooperation. What’s more, a peak in inflation and interest rates could be coming sooner than you’d think.

The Bank of England expects inflation will drop sharply from the middle of 2023. The OBR also noted the UK’s economy should grow over the coming years and while we’re struggling currently, we’re faring better than our economic neighbours.

Also, while various numbers have been thrown out, analysts expect interest rates to max out around the 5%-mark next year. Nowhere near a nightmarish 17%.

But, let’s not forget these are merely predictions. We’re all trying to find a way out of this cost-of-living crisis, but no one can predict the future.

What you can do though, is prepare your investment portfolio. Inflation typically has an impact on property prices, and you may be able to take advantage.

Source: POLITICO, Telegraph, Daily Mail, CNBC, Telegraph, Guardian, Bank of England, Gov.uk

How will the cost-of-living crisis affect house prices?

Inflation can drive house prices up, but this is just a small part of a much wider equation. Average house prices rose by 9.5% in the year to September 2022, but prices are now facing pressure. Rising costs and mortgage rates are expected to pull prices down over the coming months. Rather than see this as a negative though, it could present you with a rare opportunity to invest in property at a relative discount.

Property prices rarely stay low for long. In fact, while the OBR expects prices to fall in the short term, we’re likely to see a rebound well into the end of the decade.

Property investment, for the most part, is a long-term game. As an asset, property has proven itself resilient in the face of numerous financial crises. In April 1968, when average prices were first collated, the average property went for just over £3,500. The latest data puts the average price at nearly £295,000.

Even in the face of numerous inflationary problems, sky-high rate hikes, and economic downturns – property prices rose. We may not know the exact answer to the question ‘when will the cost-of-living crisis end?’, but you can at least prepare for better days ahead.

Disclaimer

MFS are a bridging loan and buy-to-let mortgage provider, not financial advisors. Therefore, Investors are encouraged to seek professional advice.